When preparing for the sustainability reporting process, begin by determining what components are needed within the report to make it useful, and what methods are available to measure your company’s sustainability efforts.

As mentioned in Part One of this series, there is not a single, globally accepted standard or regulation around sustainability reporting. As such, companies have the freedom to choose the framework for their sustainability report.

What are the leading reporting guidelines?

Below are the four most common guidelines, with their individual features:

- The United Nations’ (UN) Sustainable Development Goals: The UN’s Sustainable Development Goals focus on ending poverty in all forms worldwide; ensuring inclusive and equitable quality education; achieving gender equality; ensuring affordable, reliable, and clean energy for all; and promoting sustained, inclusive, and sustainable economic growth.

- The International Integrated Reporting Committee (IIRC) guidelines: The focus for the IIRC guidelines is to explain and communicate the creation of value in short, medium and long-term time frames. The IIRC recognizes six capitals including, financial, manufactured, intellectual, human, social and relationship, and natural.

- The Sustainability Accounting Standards Board (SASB) guidelines: The SASB guidelines identify and compare sustainability-related business issues with the multiple industries worldwide. The guidelines provided aid companies and organizations with determining what sustainability practices apply to their business and how to be sustainable and compliant.

- The Global Reporting Initiative (GRI): GRI is commonly accepted as most popular, author/user friendly, and appealing to stakeholders and lay persons. GRI aids companies in determining what their company or organization is materially impacting most, and where changes in operation can have the most impact, with regard to the three pillars discussed below.

The Three Pillars

After selecting a reporting framework, your sustainability report needs to address the “three pillars”: Environmental, Social, and Economic—for a balanced and long-term sustainability approach for your company:

- Environmental - When companies’ activities, systems and operations assess and attempt to reduce their environmental impact. Examples include reduction of plastics used in production and packaging, increased recycling, reduction of post-lifecycle impact for products or reduction in shipping mileage.

- Social - Represents the interactions companies have with their stakeholders, shareholders and communities. Social sustainability is the result of considering the input and needs of these groups, and the acknowledging the potential social impact of your operation locally and globally. Some ways that companies can improve social sustainability is to facilitate volunteerism of its employees, donating money to relief causes relevant to their location or work force, worker safety initiatives or participation in sustainable agriculture and food donations.

- Economic - Ensures that a company can be profitable while pursuing environmental and social sustainability. Economic sustainability refers to practices that support a long-term economic growth, without neglecting environmental and social sustainability. A company can reach economic sustainability by buying products that are responsibly and sustainably sourced, reducing overall energy demand, or staying compliant to avoid expensive violations or corrective actions.

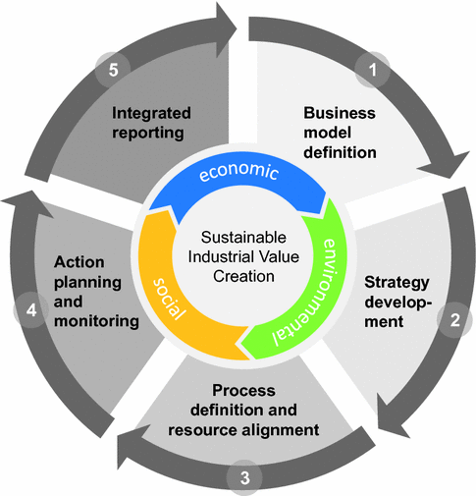

These pillars should be used to inform how sustainability will be incorporated into the various aspects or managing your business, from initial business modeling efforts and development of strategies, to defining processes, aligning resources and developing and monitoring sustainable action plans. Integrating the reporting of these aspects into routine business reporting metrics helps ensure that your company’s sustainability vision is integrated into the business.

Building Your Sustainability Platform

When evaluating each of these pillars as they relate to your operation and building a sustainability platform, there are four key components. These components include:

- Define: Define what sustainability means for your company. This should entail creating a vision of what being “sustainable” will look like in one year, three years and so on. The vision should resonate with internal and external stakeholders, and should engage employees and management. Conduct a materiality assessment that considers which issues have the biggest potential of making an impact, and which issues are the most important to your stakeholders.

- Establish: Establish sustainability goals for the company in the upcoming year, incorporating the interests of stakeholders, shareholders and other interested parties. Choose goals that align with the materiality assessment and sustainability vision, and which systems you have in place that can track progress toward meeting these goals.

- Analyze: Once goals are set, track your progress throughout the year by measuring and reporting on key performance indicators (KPIs). Collecting and analyzing hard data from each goal is the most accurate way to determine how well the goals are being enforced. Part Three of this series will provide some examples of how existing data can be used to demonstrate meaningful success in meeting sustainability goals.

- Revise: At the end of each year, goals should be added or revised to continue the sustainability of the company. Targets will help the company become more and more sustainable for many years to come while continuing to be profitable, helping their communities and helping the environment.

By aligning your sustainability goals with one of the global reporting frameworks and using the tips shown above to incorporate achievable goals into your business planning cycle, you can create a sustainability platform that not only resonates with internal and external stakeholders, but also one that produces real results in building a sustainable business.